Executive Summary:

Acorns is a mobile-first investment platform that allows users to invest their spare change. Members can also open a savings (both for adults and children) as well as an IRA account while saving money through the company’s cashback program.

Acorns makes money via subscriptions, interchange fees, management fees, and interest earned on cash.

Founded in 2012, the company has quickly risen to become one of North America’s most frequently used investment apps. So far, Acorns has raised $507 million in funding.

What Is Acorns?

Acorns is a FinTech company that offers various financial products and services, primarily in the areas of investing, spending, and saving.

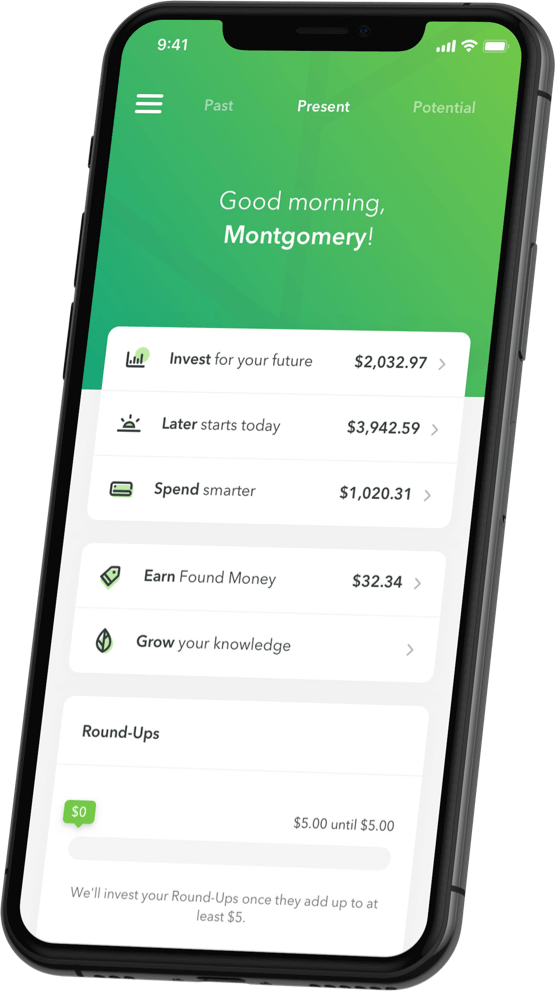

Its Invest product is a micro-investing account that allows users to invest their spare change. Acorns links directly to the user’s credit card or bank account. If, for instance, they buy a coffee for $3.50, Acorns automatically suggest the amount they could set aside (in this case $0.50) for their portfolio.

Users can create an investment portfolio within a few clicks. Acorns, depending on the user’s appetite for risk (conservative to aggressive), then invests the money into a mix of Exchange Traded Funds (ETFs). The firm will begin investing for an individual when their pool of change totals $5.

Additionally, users have the option to only invest into companies with a focus on (environmental) sustainability (the company has also planted over 700,000 oaktrees in partnership with One Tree Planted). Acorns can allocate a portion of the user’s balance towards Bitcoin as well.

With Later, Acorns sets aside a selected portion every month (starting as little as $5) and invests the money into the company’s Individual Retirement Accounts (IRA). The portfolio is selected based on the user’s age and proximity to retirement.

Later allows Acorns users to transfer payments into the IRA accounts from their taxes (transfers are treated as pre-tax income) and are only taxed as income when they retire — meaning users don’t have to be concerned about any taxable capital gains.

Acorns’ Banking product is a checking account with a debit card associated to it. Some of the account’s primary features include:

- Automatically invest spare change into the existing ETF portfolio

- Smart Deposit, allowing users to automatically set money aside before they spend it

- Being FDIC-insured up to $250,000

… and many more. The account allows users to get their checking, investment, and retirement accounts linked and displayed all in one single app.

For Earn, Acorns partners together with its so-called Found Money partners. These partners allow Acorns customers to earn cashback rewards whenever they make a purchase.

Example partners include the likes of Airbnb, Nike, Stitch Fix, Walmart, and many others. Users can either utilize their own credit cards or Acorns’ checking. Lastly, Earn is also available as a Chrome extension.

With Early, parents can open an investment account for their kids. Families can determine monthly, recurring investments that are automatically deducted from their bank accounts.

On top of that, the company has partnered with CNBC to develop educational material for families, which helps them to increase their financial literacy.

Acorns is a mobile-first company, which means that its products are primarily available via mobile applications. Users can use Acorns either on Android or iOS.

A Short History Of Acorns

Acorns, headquartered in Irvine, California, was founded in 2012 by father and son duo Walter and Jeff Cruttenden.

Walter, the father, led E-Trade’s transition into becoming an online investment platform in the late 1990s with the launch EOffering.

He also spoke frequently about investing at the family’s dinner table – and parts of that seemed to have rubbed off on Jeff.

In late 2011, Jeff began talking to his father about taking advantage of the rising popularity of smartphones. The idea was to make investing more appealing to the general public, especially since its distrust in financial institutions post the Great Depression was at an all-time high.

As a result, only 26 percent of all adults under 30 were owning stocks at all. More than 50 percent of these people simply don’t have enough money to invest, while another 30 percent state a lack of knowledge about investment opportunities as the reason.

For the next two years, the Cruttenden’s went into stealth mode and started working on the app. They even received help from Nobel Laureate and economist Harry Markowitz (who now sits on the company’s board), who’s ideas about diversifying one’s investments to minimize risk while maximizing returns have become the foundation of modern-day portfolio theory.

In March 2014, Acorns officially launched into beta. The company’s first product was Acorns Invest, which invested a user’s spare change for a minimum monthly fee.

The company first launched on Apple’s iOS store (with Android following a few months later) and instantly garnered user interest. In the first 10 weeks of the beta, Acorns was able to acquire over 10,000 users, which invested around $3/day in roundups alone.

Around that same time, the company changed up its leadership and promoted Noah Kerner to CEO. Kerner showed an interest in entrepreneurship from an early age.

At age 13, he began developing a heavy interest for DJ’ing, and was eventually working at a Super Bowl after-party, on The Tonight Show With Jay Leno, and even touring with Jennifer Lopez.

The gigs helped to fund his Cornell studies where he majored in economics and psychology. By age 28, Kerner had already started 3 companies. OneLevel, an online hip-hop culture marketplace, a music agency named Soundproof that represented artists like Quincy Jones and Babyface, and marketing agency Noise.

Noise itself was acquired by the London-based Engine Group in 2010. After that, Kerner worked with a plethora of startups to advise them on branding and marketing topics. He even invested in a selected few – one of them being Acorns.

Six months after his investment, the Cruttenden’s asked Kerner to join the company as their new CEO. He accepted on the spot.

Under Kerner’s reign, Acorns continued to exponentially grow its user base while adding many new features and products along the way. A year after the launch, Acorns even expanded into Australia (although that business has been sold off by now and rebranded to Raiz Invest).

2020, in particular, proved to be an extremely positive year. Investment activity on the platform soared due to the issuance of government stimulus checks. The company even struck a partnership with ZipRecruiter, which allowed its users to find new jobs (especially if they were laid off).

The positive outlook continued right into 2021. The GameStop frenzy, which saw online brokers like Robinhood halt trades, created thousands of unsatisfied users. Many of them decided to try out other personal finance apps – Acorns being one of them.

In the first six weeks of 2021, Acorns was able to add over 600,000 users to its platform. As a result of the firm’s growth, Acorns was able to even acquire some of its competitors, namely Harvest Platform and Pillar Life.

In May, Acorns announced that it would go public via a SPAC merger with Pioneer Merger Corp., a publicly traded special purpose acquisition company. The merger would value Acorns at $2.2 billion.

Acorns was even able to hire former Twitter and DreamWorks animation exec Rich Sullivan as its new CFO ahead of the IPO. Additionally, it appointed Seth Wunder to become its first-ever Chief Investment Officer.

Unfortunately, the tide would soon turn. In January 2022, Acorns announced that it cancelled its plans to go public due to unfavorable market conditions. Instead, $300 million in a Series F funding round were raised a few months later.

The company used portions of that cash to expand its product suite. For instance, it added Bitcoin to the portfolio of assets it invests in.

Today, Acorns serves over 11 million members on its platform, with two-thirds being subscribed to its various investment features. The company employs about 500 people working across offices in Irvine and New York.

How Does Acorns Make Money?

Acorns makes money via subscriptions, interchange fees, management fees, and interest earned on cash.

At the center of Acorn’s business model strategy stands its focus on recurring subscription revenue.

Once a customer is onboarded into its ecosystem, he or she is very unlikely to churn, especially if on a family account. After all, the average consumer in the U.S. uses their primary checking account for a total of 16 years.

The recurring subscription revenue is then being used to launch other revenue-generating features, including debit cards or browser-based coupon extensions.

And by knowing what customers are spending their money on, Acorns can offer them more tailored products that match their financial needs at the time. It, therefore, wouldn’t be unfathomable to assume if the firm eventually moves into lending and other types of financing businesses.

With that being said, let’s take a closer look at each of these in the section below.

Subscriptions

Acorns bundles its products into different subscription tiers that it offers on a monthly basis.

The Personal tier costs $3 per month and grants customers access to all of the firm’s products except the early investment account for kids.

This is where the Family plan comes in. It costs $5 per month and can be activated for as many kids as one wants.

Generating your income via subscriptions offers a variety of benefits. For once, customers willing to pay for something on a monthly basis are generally engaged with the product.

This then allows Acorns to cross-sell into ancillary services, which I’ll detail in the coming sections.

Second, customers who store money on the platform are likelier to stay on Acorns due to the hassle of moving money from one investment app to another.

As a result, Acorns can accurately forecast its revenue, which makes financial planning much easier.

The improved forecastability also makes it a much more attractive target for investors, thus allowing Acorns to accelerate growth.

Charging membership or subscription fees is fairly common among FinTech startups. Companies like Dave or Digit do derive a substantial portion of their income from charging members for access to their service.

Referral Fees

Acorns earns a referral fee whenever its members buy something at one of their 15,000+ brand partners like Nike or Walmart.

This is part of Acorns’ Earn product. Whenever a customer shops at a partner brand, they earn a percentage of the purchase price. The percentage is disclosed upfront.

The referral fee paid out is bound to the individual agreements stated in the partnership contract.

Acorns then shares a portion of that referral revenue with the member by either transferring it directly into their account or investing that money on behalf of them.

The company has vastly expanded its referral business over the past few years. For example, Acorns introduced a Honey-like Chrome extension, which grants customers access to said bonus investments.

Another referral partner of Acorns is ZipRecruiter. Users can look for employment via Acorns’ Job Finder section. Acorns then receives a referral fee for each job seeker it attracts.

And there is no shortage of additional monetization options. For example, it could introduce insurance or mortgage comparison features.

Interchange Fees

Users can apply for a checking account that comes with a free debit card. The card itself is issued in partnership with Visa.

The account is FDIC-insured all the way to $250,000 and offers free ATM retrievals, built-in smart deposits, and more.

Interchange rates are dependent on a variety of factors, including the type of card (debit vs. credit), location, and what is being purchased.

Visa interchange rates in the United States are normally equal to around 0.50 percent + $0.10 in fixed fees.

Interchange revenue is a common monetization tactic among FinTech startups. Companies like Chime do derive a substantial portion of their income from interchange fees.

Management Fees

Acorns charges an annual management fee of 0.25 percent for accounts larger than $5,000. This covers the time and effort it takes to choose the best investment opportunities for any given user.

For any member that has less than $5,000 in their account, the management fee is lifted. Instead, they will pay one of the subscription fees highlighted above.

The fee is largely in line with competing products like Betterment and Wealthfront, which also charge 0.25 percent.

Interest On Cash

Acorns, just like any normal bank, uses the unused cash residing on its user accounts to generate interest income.

It deposits said cash into interest-bearing bank accounts on which it then generates income.

The company incentivizes users to keep their cash in its cash accounts by paying interest.

Consequently, those interest fees are lower than what the firm generates from the cash it deposits.

Furthermore, Acorns utilizes various techniques grounded in behavioral economics (e.g., saving a lower amount every day vs. larger sums on a monthly basis) to grow the cash balances of its users.

Again, the greater those cash balances are, the more income from interest fees Acorns can derive.

Acorns Funding, Valuation & Revenue

According to Crunchbase, Acorns has raised a total of $507 million across 11 rounds of venture capital funding.

Investors into the company include the likes of TPG, BlackRock, PayPal, Bain Capital Ventures, NBCUniversal, DST Global, and even stars like Kevin Durant or Jennifer Lopez.

Right now, Acorns is valued at $1.9 billion. The firm was previously valued at $2.2 billion during its SPAC merger with Pioneer Merger Corp., initially announced in May 2021, which was ultimately abandoned.

As a (still) private company, Acorns is not obligated to disclose its revenue. But multiple reports in the past have indicated that the company’s annual revenue is closing down on about $100 million.