Executive Summary:

N26 is direct bank offering various financial products through its mobile application. Its main differentiator from traditional banks is a technology-first approach to banking, no physical branches, convenience of service, free accounts, and a transparent fee structure.

The business model of N26 is based on charging private consumers or business owners for premium subscription plans. Other channels of income include overdraft fees, interest paid on loans, cashback programs, interchange fees, interest on cash, and commission fees for insurance sales.

Founded by two novice entrepreneurs, N26 became one of the highest funded and valued startups out of Europe. Having raised over $680 million to date, the company was able to acquire over 5 million customers worldwide.

How N26 Works

N26 (formerly Number 26) is a German direct bank that offers various financial products to consumers. As a direct bank, the company does not operate any physical branches, but provides all its services remotely through its mobile app.

Registration and authentication for accounts occurs fully online. Users can expect to fulfill the registration process in less than 15 minutes.

Once registered, users can order a physical credit card at different price points (more on that later). The card enables payments at physical stores.

Other features on the app and service include:

- Multiple savings accounts called Spaces

- Budgeting tools to organize spend

- Transferring money to other domestic and international accounts

- Rewards for card usage

- Purchasing and managing your private insurances

Lastly, the account can also be used by business owners and freelancers. These accounts come with additional features such as company expense management or printing the transactions list for taxes.

A Short History Of N26

N26 was founded in 2013 by Valentin Stalf (CEO) and Maximilian Tayenthal (CFO). Tayenthal, at that time, was busy finishing up his law PhD at the university of Vienna. Stalf, on the other hand, already got his entrepreneurial feet wet by building various businesses for German startup incubator Rocket Internet.

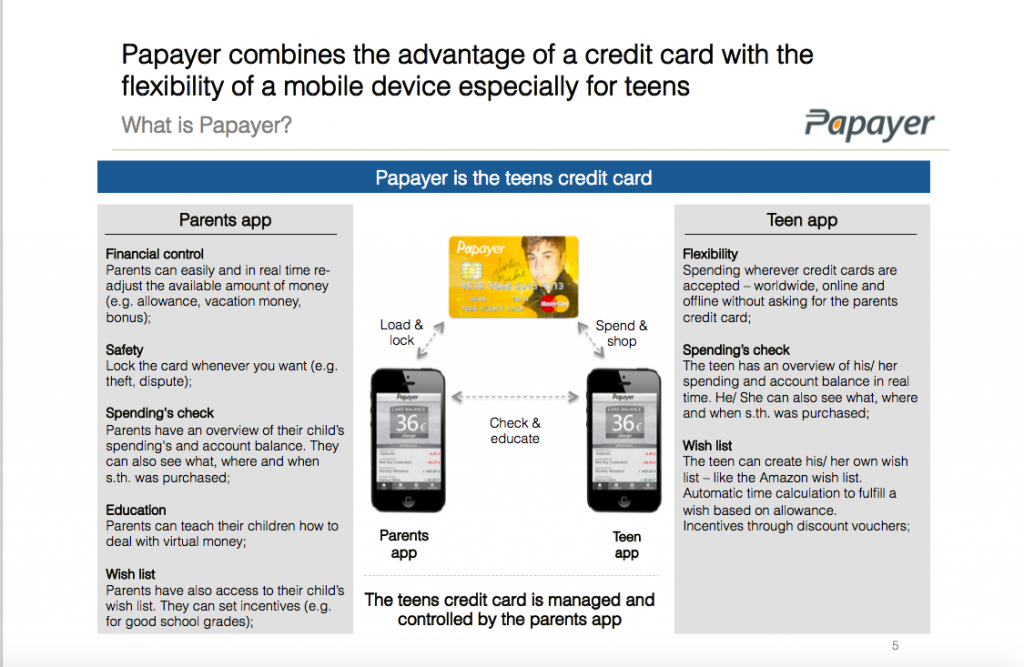

In 2013, the pair decided to take the plunge and start their own business. N26 initially started out as Papayer (based on the papaya fruit) and was intended to be a prepaid credit card for teenagers.

The initial revenue model also differed compared to how N26 operates today. Initially, the team wanted to charge a one euro fee per withdrawal. The app would allow parents to manage their kids expenses.

An early pitch at Axel Springer’s Plug & Play accelerator program led to an investment of €150,000. With that money, the founders were able to develop the initial version of their app.

What they discovered early on was that teenagers weren’t really engaging with the product as much as the founders hoped. What came at a much bigger surprise was the fact that their parents were the ones who were heavily involved.

At that time, no other mobile banking solution was around. So the parents used the app for tasks such as budget monitoring and peer-to-peer money transfers.

The founder quickly realized that the opportunity (and addressable market) was much bigger than expected. They quickly pivoted into a new model and name, and in 2014, Number 26 was born.

That same year, they moved the company from Vienna (where Stalf and Tayenthal are from) to Berlin. Furthermore, they formed a cooperation with Wirecard to offer the MasterCard for their adult customers.

Number 26 launched in 2015..The company became instantly popular due to its modern design, quick signup time (setting up a bank account takes 10 minutes) and free accounts. That same year, Peter Thiel’s Valar Ventures invested another $10 million into the company to help fuel growth.

In 2016, the company again rebranded into N26 to make it more appealing to its rising international customer base. That same year, they received their own banking license, becoming the first European mobile bank.

Nevertheless, the aggressive growth has had its hiccups. For instance, various bank accounts had been comprised in a hacking attack, leading to money being stolen. Other users were not able to access their accounts for weeks. The company responded by opening a security lab in Vienna, which will focus on improving the safety of the application.

How Does N26 Make Money?

Although N26 (and its competitors) is perceived as one of the biggest threats to traditional banks, the way they make money is fairly similar to their traditional counterparts.

Let’s look at the ways in which N26 makes its money.

Subscription Revenue

The primary source of income are the different subscription plans offered to both private consumers and business owners.

In the private consumer space, N26 offers three different plans:

- The basic plan is free of charge

- The N26 You plan comes at €9.90 a month, including additional benefits such as an extra card, insurance and discounts at partner stores

- The N26 Metal plan costs €16.90 / month and offers a few more benefits, for instance priority customer support and exclusive access to Metal Experiences

On the business side, two more plans are offered:

- A free basic plan

- N26 Business You including (€9.90 / month) no ATM fees in any currency, 0.1 percent cashback, insurance, selected discounts or an extra card

Lastly, the different plans come with a different type of card, from a plastic (basic plan) to a metal (N26 Metal) card.

Interchange Fees

For every successful physical card transaction made, N26 (and MasterCard) will take a cut.

Although not publicly disclosed, the commission should be in line with standard MasterCard charges. N26 and MasterCard would then share the commission, which should total around 2 percent.

Overdraft

Customers can receive up to €10,000 in overdraft. If the account is in the negatives, consumers have to pay an overdraft fee for extending their limit.

N26 applies an 8.9 percent interest rate on the overdraft balance.

Insurance Commission

N26 offers a set of insurance plans through its collaboration with insurance robo-advisor Clark. Some of the plans include:

- Liability

- Legal

- Household

- Automotive

- Health

- Disability

… and many more. In the insurance case, N26 acts as a mediator and lead generator for traditional insurance brokers.

Other Case Studies Worth Your Time: The Lemonade Insurance Model

No public information has been disclosed on this topic, but in the most likely case N26 receives a percentage commission for every insurance booked through its app.

Loans

Through its N26 Credit unit, the company offers personal loans between €1,000 and €50,000. Repayment can take between 6 to 48 months.

N26 earns money on the interest charged for the loan. The rate lies between 1.99 and 19 percent per year.

Cashback

N26 partners with other companies, such as Lime, Booking or Headspace, to offer cashback incentives for completed purchases.

When completing a transaction at one of their partners with their N26 account, customers receive various discounts.

Although the deal structure is not publicly disclosed, it can be assumed that N26 receives a commission on every successful transaction made through the cashback program.

Interest On Cash

N26, just like any normal bank, uses the cash residing on user accounts to lend it out to other institutions, such as said banks.

They then collect interest from these institutions (also called Net Interest Margin). For 2019, according to Statista, net interest margin for all U.S. banks was equal to 3.35 percent.

N26 Competitors

N26 offers bank accounts in 26 different countries across Europe and North America. As such, the company competes not only against other FinTech startups, but also local and traditional banks.

Let’s look at some of the stiff competition N26 is facing.

Monzo

Monzo, a FinTech out of London, was founded in 2015 by Tom Blomfield (CEO), Tom Foster-Carter (COO) and others. It offers a variety of banking solutions such as bank accounts, savings and borrowing options, or purchasing energy plans.

Monetization occurs through subscriptions for premium or business accounts, interest on loans and commission (e.g. when purchasing an energy plan).

Like N26 (and frankly all other mobile banks), Monzo’s account comes with a Mastercard, which is directly connected to the mobile app.

Its last Series F funding round valued the company at $2.5 billion. As of December 2019, over 3.5 million people registered for a bank account. Currently, the company is active in its UK home market as well as the USA.

Revolut

Revolut, headquartered in London, was founded in 2015 by Nikolay Storonsky (CEO) and Vladyslav Yatsenko (CTO). Next to a digital bank account, the company offers solutions such as digital peer-to-peer payments, trading options and budgeting tools.

Like N26, Revolut monetizes customers through premium monthly subscriptions. Furthermore, they take a fee on any international payment or stock purchase.

As of today, the company has raised over $836 million in funding while being valued at $5.5 billion. Revolut is available in over 30 countries worldwide, making it the biggest player in the neobank space.

Chime

Chime, founded in 2013 by Chris Britt (CEO) and Ryan King (CTO), is a digital bank out of San Francisco.

As of today, it offers a personal bank account with different features such as no hidden fees, getting paid early or automatic savings. Its biggest appeal compared to traditional US banks is the lack of fees involved.

As opposed to other banking FinTech’s, Chime only makes money by collecting fees from their Visa card. Hereby, the merchant or seller of the product is charged, and not the customer itself.

As of today, the company counts over 8 million customers. It raised over $800 million in funding, valuing it at $5.8 billion.

Starling Bank

Starling Bank, founded in 2014 by banking veteran Anne Boden (CEO), is another challenger bank out of London, UK. It offers current as well as business banking accounts. Furthermore, users can apply for loans and send money to other, both domestically and internationally.

Starling puts an emphasis on social good and sustainable growth. As such, ¼ of the company is still owned by the founder and employees.

N26 Valuation, Revenue, Ownership & Growth

According to Crunchbase, N26 has raised over $680 million in seven funding rounds. During its last round of funding (extension of its Series D round) in July 2019, the company raised another $300 million, valuing them at $3.5 billion.

Investors into the company include Tencent, Earlybird Venture Capital, Allianz X, Insight Venture Partner’s and Peter Thiel’s Valar Ventures. The capital, as typical for growth companies, will be deployed into market expansion (i.e. Brazil), product improvements and new hires.

The company has not shared any official revenue numbers as of today. As of January 2020, N26 claimed over 5 million customers in total. Earlier in 2019, 2.5 million customers held €1 billion in their N26 accounts overall. Furthermore, the FinTech processed over €20 billion in transaction volume since its inception.

As of July 2019, the founders still own over 20 percent of the company. Taking their last private valuation as a basis, that ownership stock would be equal to about $700 million.