Executive Summary:

Revolut is a neobank offering various financial products to consumers and businesses. It does so through its mobile application, which is available on iOS and Android devices. As a neobank, Revolut does not operate any physical branches.

Revolut’s business model is based on several levers, including different subscription plans (for both consumers and businesses), fees for international transfers and withdrawals or interest and overdraft paid on loans. Furthermore, it offers additional financial products such as trading, various insurances as well as a cashback program.

Founded by two Russians with vast experience in the financial sector, Revolut quickly became one of the world’s highest funded FinTech start-ups. Today, the company counts over 10 million users, 2,000 employees and operates in close to 30 countries across the globe.

How Revolut Works

Revolut is a British neobank that offers various financial products via its mobile application. The service is accessible via iOS and Android. As a neobank, Revolut is digitally enabled and therefore does not operate any physical customer branches.

Registration for the account occurs via online identification. Customers can normally expect to receive their account within a matter of minutes. The physical card, depending on location, follows a couple of days later.

The physical card is directly connected to the digital account on the mobile phone. Once a payment or transaction is made, it becomes instantly visible in the app.

Other features include:

- Transferring money to other users or bank accounts (both domestically and globally)

- Creating budget plans to manage funds (along with spending dashboards)

- Vaults to automatically put money aside for saving purposes

- Trading different stocks or investing in crypto currencies

- Buying various insurances, or getting a concierge to book and organize trips for you

- Donating to various organizations such as the WWF

Business owners and freelancers can use Revolut as well. Next to the features seen in the consumer account, other functions include for instance various tools for accounting purposes, API integrations or corporate cards.

Make Some More Time To Read About Revolut's Biggest Competitor

A Short History Of Revolut

Revolut was founded in 2015 by Nikolay Storonsky (CEO) and Vladyslav Yatsenko (CTO). Prior to starting Revolut, Storonsky spent 7 years as a financial trader at Lehman Brothers and Credit Suisse respectively.

In 2013, he left his lucrative trading job as he became increasingly frustrated with the regulations and changes in behaviour prevalent after the financial crisis.

Yatsenko, on the other hand, had over 10 years of practical experience building software products in the financial sector. He worked as a software engineer for the likes of Deutsche Bank, UBS and Lab49.

Revolut initially started out as a money exchange service. Storonsky, who often travelled frequently during his trading days, recalled in an interview with Forbes that “he was travelling a lot and wasting hundreds of pounds on foreign transaction fees and exchange rate commissions which just didn’t feel right.”

Initially, Revolut came out of Level39, a start-up accelerator tailored towards the creation of FinTech products.

Soon after the launch in February 2015, the company was able to successfully raise its seed round of $2.3 million led by Balderton Capital and Seedcamp. This came on the backbone of over 1.5 million recorded transactions and weekly growth of up to 30 percent.

In 2018, Revolut was able to secure a specialised banking license issued by the European Central Bank (facilitated by the Bank of Lithuania). This allows the company to accept deposits and offer consumer credits.

Nevertheless, Revolut’s growth hasn’t been without controversies. In 2019, Wired Magazine published an article on the gruesome working conditions and mistreatment of employees.

Weeks later, the company’s CFO Peter O’Higgins resigned after allegations that the company turned off an anti-money laundering system that protects users from fraudulent transactions.

All these roadblocks haven’t slowed down growth though. Today, the service is present in close to 30 countries and counts over 2,000 employees worldwide.

How Does Revolut Make Money?

While Revolut’s core banking account is free of charge, there are a multitude of other products and services with which users are monetized.

Let’s look at the various income streams of Revolut in more detail.

Subscription Revenue

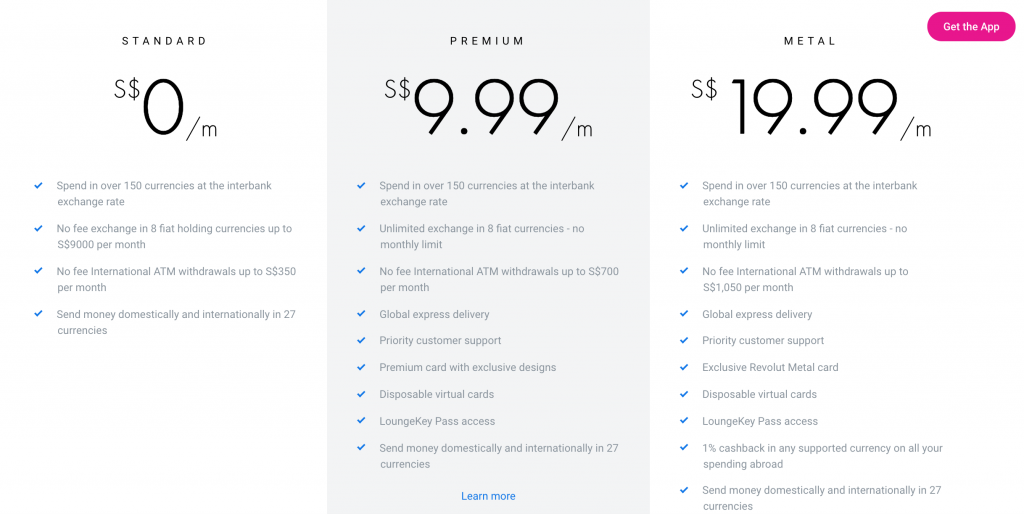

Revolut offers three different plans for consumers. These include Standard, Premium and Metal.

While the Standard plan is free, consumers will have to pay for the other two. The paid plans come with additional features and services, including:

- A premium card with elevated design (a metal card is given out for the Metal plan, duh)

- Prioritized customer support

- Withdrawing cash without fees for up to $900

- Free lounge passes for delayed flights

- Cashback

… and many more.

Interchange Fee

For every successful physical card transaction made, Revolut (and MasterCard) will take a cut (called Interchange Fees). Although not publicly disclosed, the commission should be in line with standard MasterCard charges.

Revolut and MasterCard would then share the commission.

International Money Transfers

Customers can transfer up to £5,000 abroad every month for free. For anything above this amount, a fee of 0.5 percent is applied to the transaction.

For customers opting in for the paid plans, the monthly limit is higher.

Perks

When paying with your Revolut card at one of the selected partners, customers will receive a discount if a customer records ten successful transactions.

While this program is still in the beta testing phase, it is already known that partners will come from industries such as travel, dining, groceries, shopping or entertainment.

Depending on the agreement, Revolut will most likely receive a cut on every payment made through its card.

Insurance

Revolut users can buy two types of insurances, namely being device and overseas medical insurance. Revolut offers these insurance packages through its subsidiary called Revolut Travel Limited.

Here's Another Startup Revolutionizing The Stone Age Insurance Industry

Revolut Travel Limited acts as an auxiliary insurance intermediary of Simplesurance GmBH (for device) and White Horse Insurance Ireland (for travel). Therefore, the insurance services will be provided by Simplesurance and White Horse Insurance.

Revolut will hereby take a percentage cut for facilitating the purchase of the insurance.

Trading

Through its Revolut Trading LtD subsidiary, the company is providing the possibility to buy and sell stocks from various companies.

Standard and Premium plan customers are allowed to trade 3 and 8 stocks respectively per month. When exceeding this amount, a flat fee is applied for every additional transaction. For British users, this fee is 1 GBP.

Metal card holders, on the other hand, don’t have any limitations and can trade unlimited amount of stocks.

Loans & Overdrafts

Customers can furthermore opt in for loans. These loans range from £500 up to £25,000 while the repayment period is between 12 to 60 months.

Revolut makes money by the interest it collects for each loan. The interest fee depends on the customer’s credit score, the amount as well as length of the loan.

If a customer is late for his/her payment, an additional overdraft fee is applied as penalty.

Business Accounts

Similar to the customer subscription, businesses and freelancers respectively can opt in for different subscription plans.

Example features include:

- Expense management tool to manage your employee’s spending

- Bulk payments

- Employee perks at partners such as Amazon or Starbucks

- Open API to connect to your accounting software

- Assign roles and permissions to different employees

Similar to the consumer plans, subscriptions can be cancelled at any time.

Interest On Cash

Revolut, just like any normal bank, uses the cash residing on user accounts to lend it out to other institutions, such as said banks.

They then collect interest from these institutions (also called Net Interest Margin). For 2019, according to Statista, net interest margin for all U.S. banks was equal to 3.35 percent.

Revolut Funding, Revenue & Valuation

According to Crunchbase, Revolut has raised over $836 million in 14 rounds of funding. In its latest funding round (Series D), Revolut was able to $500 million at a $5.5 billion valuation.

For the fiscal year of 2018, Revolut reported revenues of £58m (roughly $75 million) with pre-tax losses of £33 million. Revenue for 2019 is expected to triple according to Revolut COO Richard Davies.

Investors into Revolut include the likes of Lakestar, Index Ventures, DST Global, Greyhound Capital, Global Founders Capital and many others.