Executive Summary:

Upstart is a digital lending platform that utilizes artificial intelligence to give customers access to affordable credit.

Upstart primarily makes money via the fees it imposes on its partners as well as interest from loans it personally issues.

Founded in 2012, the company is now one of the fastest-growing FinTechs in the United States. In late 2020, Upstart went public on the Nasdaq stock exchange.

How Upstart Works

Upstart is a digital lending platform that utilizes artificial intelligence (AI) to give customers access to affordable credit.

The company works together with dozens of banks that are the actual issuers of the loans that consumers can apply for.

Traditionally, banks have utilized the FICO model to assess the risk of someone’s credit default. However, since FICO is a scorecard-based model, it poses various limitations. For example, it does not take rent and other types of potentially relevant data into account.

Additionally, the model often discriminates against people of color and those with large sums of debt who may actually be qualified for loans (such as medical students).

Not only does this lead to limited access for borrowers but vastly increases the risk of the banks that issue the loans.

Upstart claims that its AI-based model allows lenders to approve almost twice as many borrowers all while leading to fewer defaults. Additionally, borrowers pay less interest (APR) due to the accuracy of Upstart’s models.

Customers can apply for all kinds of loans, ranging from personal loans for weddings or home improvements all the way to small business and car refinance loans.

The loans that Upstart facilitates normally range between $1,000 to $50,000 at interest rates of 7 percent to 36 percent, which is essentially in line with competitors such as Lending Club or SoFi.

Consequently, Upstart works together with a variety of lenders, namely banks, credit unions, and even car dealerships.

Upstart, since it was first launched back in April 2012, has originated close to $30 billion in loans – 73 percent of which have been automatically issued by its AI systems.

Detailing The Founding Story of Upstart

Upstart, headquartered in San Francisco, California, was founded in 2012 by Dave Girouard, Paul Gu, and Anna M. Counselman.

To say that CEO Girouard has experienced the highs and lows of the Valley is probably an understatement. After graduating from Dartmouth back in 1988, he joined Accenture as a consultant.

He subsequently pursued his MBA at the University of Michigan, which he wrapped up in 1993. Over the coming decades, he held executive positions at firms such as Booz Allen & Hamilton, Apple, and Virage.

Girouard ultimately joined Google in 2004 where he was responsible for building up its Enterprise division, which entailed products such as Gmail. When he ultimately left in 2012, he had risen to become the division’s president, thus overseeing all product development.

Funny enough, his financial adviser discouraged him from pursuing his own business due to the money he was potentially leaving on the table if he were to depart from Google.

However, being driven by the passion to branch out on his own, he was determined to somehow make it work. He managed to convince Anna Mongayt Counselman, who was also working in Google’s Enterprise division, to join him.

At Google, Girouard managed a team of 1,000+ people and would repeatedly receive tens of thousands of job applications – every week. His team even had to develop software to algorithmically process and weed out the best candidates.

“We can look at a 25-year-old and very quickly assess whether he or she would be successful at Google,” he recalled during an interview with Xconomy. “My whole thesis was, if you could use the same algorithms to predict whether he or she would be successful beyond that, in the business world, that would be pretty useful.”

Unfortunately, he wasn’t sure how to turn that insight into a viable business. In the beginning, Girouard planned to create an auction-style system on which applicants would create personal profiles and let investors decide how much they were worth. Luckily, a young student on the other side of the country had a better idea.

In 2011, Paul Gu dropped out of his Computer Science studies at Yale after he was accepted into the Thiel Fellowship. The program launched by the controversial PayPal founder supports young college or high-school dropouts with $100,000 in seed funding to pursue their dreams.

Gu first tinkered around with a local-commerce startup, which quickly fizzled out. Soon after, he began experimenting with regression models that would predict a person’s future income and fund those people accordingly.

His motivation was grounded in the experience of Gu’s friends. Many of them, due to crippling student debt, had to take on jobs they didn’t particularly enjoy. Girouard got wind of what Gu was working on and invited him to fly out to San Francisco, which he immediately did.

“As soon as I saw what he was doing, I thought why the hell do an auction? Let’s just price this ourselves and we can build a model without burdening the backers,” Girouard told GigaOM.

And just like that version #1 of Upstart was born. Founders could apply for personal loans in exchange for a percentage of their future income. The payments were made on a monthly basis and would be verified based on the borrower’s annual tax returns.

However, in order to incentivize founders, payments would be capped at a 14.99 percent annual return of the investment. The loans themselves would actually not be issued by Upstart but by outside backers. Upstart was essentially the in-between layer, something that it stays true to even today.

In order to grow the company, Upstart still needed some capital, which came in the form of a $1.75 million seed round led by Kleiner Perkins, with participation from Google Ventures, NEA, and Dallas Maverick’s owner Mark Cuban.

The funding, furthermore, allowed Upstart to hire its first few employees, many of whom had previously worked together with Girouard at Google.

Within the first 8 months of operation, the company managed to issue loans worth over $1 million. Some of those founders, such as Catarina Spear of FIGS, ended up creating companies that are now worth tens of millions of dollars.

The early success allowed the founders to raise $5.9 million in Series A funding back in April 2013. However, just a year after the funding round, the team decided to pivot into what it felt was a substantially more lucrative model.

Inspired by the success of companies like Lending Club or Prosper, Upstart pivoted towards becoming an investor marketplace that would offer three-year standard term loans available in all 50 states.

Borrowers, once verified, could request loans of up to $25,000 at interest rates between 6.5 percent to 20 percent APR. Furthermore, they could use the money to pay off literally anything, ranging from credit card debt to tuition fees.

Upstart also partnered with 13 coding bootcamps, which borrowers could apply for. The money itself, just like with the previous model, would be provided by individual and accredited investors.

To support the pivot, the founders raised another $18.9 million in Series B funding led by Khosla Ventures. Meanwhile, interest in its business model only accelerated when Lending Club filed to go public towards the end of 2014, thereby becoming the first online lender to do so.

Once the model was proven, Upstart decided to scale it by partnering with institutional investors instead of private individuals. Asset management firm CPV, in April 2015, for example, increased its investment in Upstart loans from $100 million to $500 million.

Venture investors certainly were digging the B2B approach as well. In July of the same year, they poured another $35 million in Series C funding into Upstart. The funding even allowed Upstart to snatch away high-level executives such as Uber’s growth marketing chief Mike Osborn who became the firm’s first CMO.

Upstart largely remained outside the limelight to focus on growing the core business. That all changed when, in March 2017, it announced another fundraise of $32.5 million to fuel its growth trajectory.

Over the previous 2.5 years, the company issued loans worth $650 million. Moreover, 25 percent of them were fully automated. For reference, Lending Club had issued loans totaling $26 billion at that point.

The more important news was announced in September of that same year, though. The Consumer Financial Protection Bureau (CFPB) sent shockwaves across the lending industry when it issued a no-action letter to Upstart.

A first among FinTech companies, it granted Upstart a break from regulatory enforcement. This meant that the company could utilize alternative data, such as a person’s cost of living, to make borrowing and pricing decisions. In turn, Upstart committed to regularly reporting performance and inclusivity data.

By the beginning of 2019, Upstart had already facilitated loans worth over $3 billion. Yet again, its growth was rewarded with another funding round. In April, it raised $50 million in Series D funding led by Progressive Investment Company. Investors in the round valued Upstart at $750 million.

Unfortunately, not everything was always going according to plan. In February 2020, senators Sherrod Brown and Elizabeth Warren, along with three other representatives, accused Upstart of not complying with fair-lending laws.

More precisely, they cited a report by the Student Borrower Protection Center which stated that Upstart was charging higher interest rates to students from historically black or predominantly Hispanic colleges.

However, the study itself was highly questionable. It was essentially based on one single person requesting a loan 26 different times. Co-founder Paul Gu highlighted that Upstart conducts “rigorous and quarterly fair-lending testing across millions of actual applicants.”

To make matters worse, the Covid-19 pandemic led to a significant decrease in revenues as banks stopped issuing loans. Luckily, those woes largely subsided as the United States government began printing money like there was no tomorrow.

The boost in revenue gave the founders the confidence to take Upstart public, which they ultimately did in December 2020. The IPO added another $240 million to the firm’s balance sheet. Interestingly, the filing also revealed that close to 70 percent of Upstart’s revenue was derived from one single banking partner (Cross River Bank).

Being a public company certainly adds a lot of creditability to your brand. Upstart benefited from the increase in recognition by being able to sign up even more banking customers.

It also used the money to make its first-ever acquisition. In March 2021, it bought Prodigy Software, a provider of cloud-based automotive retail software. It used Prodigy’s existing customer base to launch Upstart Auto Retail in October, allowing both dealerships and manufacturers to issue loans to consumers.

Over the course of the coming months, Upstart continued to double down on its automotive division. It even issued loans itself, simply to get the ball rolling. Manufacturers like Subaru and Volkswagen would, however, also become customers not long after the launch.

Unfortunately, cloudier times would soon be on the horizon. The ensuing recession once again forced banks to issue fewer loans to minimize risk. And it certainly did not help that interest rates, due to inflation, were raised simultaneously.

Meanwhile, Upstart decided to terminate its relationship with the CFPB because it wanted to expand the number of parameters it includes within its loan assessments.

Law firm Relman Colfax, which was hired by Upstart to monitor its fair-lending compliance, added to the firm’s troubles. In September 2022, it issued a report which stated that Upstart indeed was issuing fewer loans for people of color.

How Does Upstart Make Money?

Upstart primarily makes money via the fees it imposes on its partners as well as interest from loans it issues.

Upstart essentially operates under a two-sided marketplace business model, meaning it connects borrowers (you and I) with lenders including banks or other financial institutions.

As a result, it is not Upstart but the partner who underwrites the loan. But why would a bank take on all that risk and not just issue the loan itself?

The answer is because Upstart is substantially better at assessing the risk of a given borrower and loan.

As previously stated, the FICO-based model is not necessarily a great predictor of the risk a borrower poses. Upstart, on the other side, takes more than 1,500 parameters into account to assess said risk.

Additionally, the firm has analyzed billions of data points throughout its existence, which consequently improves the accuracy of its machine learning-based models.

In the meantime, relying on AI also decreases Upstart’s cost base. 2.5 years into the lending business, it processed 25 percent of all loan applications automatically. Today, that number has risen to 73 percent, thus significantly speeding up decision making all while decreasing the need for human involvement.

Furthermore, most of the banks that Upstart partners with are small ones that don’t employ an army of statisticians. The bigger players, like Goldman Sachs or Morgan Stanley, have long moved on from solely relying on FICO-based credit assessments.

And as more banking partners are onboarded, more and more data are being analyzed, which consequently improves accuracy and thus minimizes risk for all participants in the network.

This trained data can be and is being utilized to expand into additional segments as well. As stated above, Upstart launched an automotive division in October 2021 and plans to expand into mortgages sometime in the future.

Similarly, Upstart announced a partnership with NXTsoft, which provides API connectivity for banks, in June 2021. The partnership enabled Upstart to more efficiently implement its models at any U.S.-based financial institution.

Lastly, another major benefit of its model is that, unlike a traditional bank, Upstart does not operate any costly physical branches.

Instead, it can take advantage of the traffic its website generates. Upstart also offers a white-label solution for banks, which means they can utilize its technology on their own website when offering loans.

So, without further ado, let’s take a closer look at each of Upstart’s revenue streams in the section below.

Fees

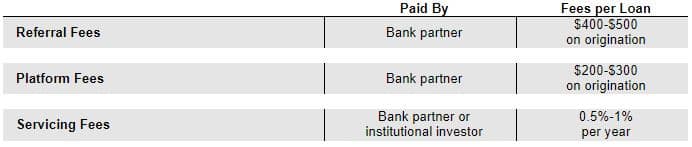

The overwhelming majority of revenue that Upstart generates comes from the various fees it charges to its automotive and banking partners.

More precisely, the firm imposes three types of fees, namely referral fees, platform fees, and servicing fees.

The referral fee is paid whenever a loan is referred through Upstart.com and originated by the banking partner. Consequently, the referral fee is charged on a per-loan basis.

Platform fees are essentially loan origination fees, which normally range between 5 percent to 8 percent and are paid by the consumer to the bank, which in turn pays Upstart.

The platform fees cover the various costs that Upstart incurs. These include verification and fraud detection, the collection of loan application data, and more. Similarly, platform fees are applied whenever a new loan is issued.

Lastly, banks and other partners pay loan servicing fees of 0.5 percent to 1 percent on all outstanding loans. The fees are paid on an ongoing basis.

It has to be noted that the above-stated fees are paid by its banking partners. The fee structure that applies to its automotive lenders is currently not being disclosed.

Interest

Another, albeit very small, revenue stream is the interest that Upstart collects on the loans it originates itself.

As stated above, the firm has been issuing loans when it launched its automotive division to essentially get the ball rolling and tweak the offering.

In recent times, Upstart was criticized by investors for the fairly large sum of loans (~ $600 million) on its balance sheet. After all, it increases the firm’s operating risk.

More importantly, it is in Upstart’s best interest to not become a direct competitor to its biggest customers, namely the banks.

“We’ve said we use putting loans on our balance sheet to test new products and new models, and that’s largely what those represented,” Girouard told CNBC in response to the criticism the firm faced.

Weeks after the controversy, Upstart CFO Sanjay Datta announced that the firm would no longer keep loans on its balance sheet which financial institutions are not attracted to purchase.

It has to be noted that risk, with more than $800 million on its balance sheet all while running a fairly profitable business, still remains somewhat moderate, though.

Upstart Funding, Revenue & Valuation

Upstart, according to Crunchbase, has raised a total of $144.1 million across 7 rounds of venture capital funding.

Investors in the company include Rakuten, Khosla Ventures, First Round Capital, Third Point Ventures, and many more.

Upstart raised another $240 million when it went public back in December 2020. At the time, it was valued at $1.8 billion.

During the fiscal year 2021, Upstart generated $849 million in revenue, up 264 percent from 2020 ($233.4 million).