Remember when your parents told you to never get into a stranger’s car? Well, it’s 2022 and that’s what you and everyone else are doing now.

That revolution has been ushered by Uber Technologies, or Uber, which grew from a timeshare limo service in San Francisco to now over 70 countries and billions in annual revenue.

In the process, the company has not only angered taxi operators and governments but even its own employees, which even lead to the resignation of its founder and CEO Travis Kalanick back in 2019.

The adults have since taken over Uber, which is now widely considered the world’s leading ride-hailing and even transportation platform. But how has it managed to create this juggernaut of a business?

In short, Uber possesses four distinct competitive moats, namely network economies, process power, branding, and counter positioning.

We will be analyzing Uber’s competitive advantages through the lens of Hamilton Helmer’s 7 powers, which detail how companies are gaining an edge over their contemporaries.

World-renowned tech executives including Reed Hastings (founder and CEO of Netflix) as well as Daniel Ek (CEO and founder of Spotify) have leaned on Helmer’s framework to devise the strategy for their respective businesses.

The 7 powers include: scale economics, switching costs, cornered resource, counter positioning, branding, network effects, and process power.

However, I will only analyze the powers that are applicable to Uber’s business. Scale economies, for example, are normally how manufacturing companies producing physical components separate themselves from the pack.

So, without further ado, let’s take a closer look at each competitive advantage that Uber possesses.

1. Network Economies

The single biggest competitive advantage that Uber possesses is the network economies it has amassed.

Network effects improve the experience and value of a service with each new member that joins it. A classic example would be a social platform like LinkedIn. Each new user that joins allows others to connect with potentially more people for all kinds of purposes (e.g., finding jobs or advertising a service).

In the case of Uber (the ride-hailing platform), it operates a two-sided marketplace that connects drivers with people wanting to go from A to B (= riders).

Uber essentially benefits from what one would call hyperlocal network effects. The addition of a new driver only improves the service for someone living in the same location. An additional unit of supply (= driver) in New York City wouldn’t necessarily affect your experience if you were from Los Angeles.

As a result of the local nature of its marketplace, Uber needs to invest heavily in driver acquisition whenever it enters a new city.

During its first few years of operation, it spent hefty sums of (mostly investor) money to incentivize drivers to join. In one instance, a UK-based driver was making over $20,000 a month in referral fees from bringing on new drivers.

However, the referral fees were only paid out if the new driver completed a minimum of 25 trips in their first 30 days on the platform. This seemed to be the sweet spot to get drivers to offer their services regularly.

Additionally, the fees Uber was charging were also much lower than they are today (around 30 percent, on average). In some rare cases, it was paying taxi drivers over $1,000 to lure them away from their employers.

Similarly, the company was offering $20 or more to new riders to incentivize them to try out the service.

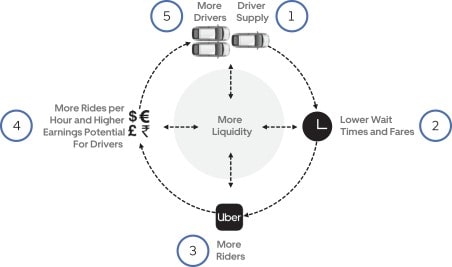

Uber itself made sure to point out the importance of its network economies within its S-1 prospectus, which it filed before going public in May 2019.

“Our strategy is to create the largest network in each market so that we can have the greatest liquidity network effect, which we believe leads to a margin advantage,” the prospectus read.

Liquidity, in this context, refers to Uber’s ability to satisfy demand when it arises. The platform’s sweet spot is around 5 minutes of waiting time for the rider.

Creating a liquid network, as seen above in the picture, offers advantages for both drivers and riders. Drivers benefit from steady work, which translates to higher earning potential. Riders, on the other hand, pay lower fares and have lower waiting times.

The great user experience (i.e., low waiting times, better prices compared to taxis) then prompts more customers to sign up, which in turn incentivizes additional drivers to join. As a result, the network eventually takes on a life of its own once it hits critical scale.

It has to be noted, though, that Uber also suffers from negative network effects. For instance, an additional unit of driver supply makes the platform more competitive for existing drivers, which in turn decreases their ability to charge competitive rates.

Similarly, while additional riders may strengthen the earning potential of drivers, they also lead to higher costs for people seeking rides (as the marketplace becomes more competitive).

Hence, Uber continues to emphasize that its optimal equilibrium is somewhere around the 5-minute mark. After all, many riders (at least speaking from personal experience) are probably still getting ready while ordering a car, which would push waiting times into a few minutes.

There are two more aspects where Uber benefits from the network effects it has amassed. The first one is defensibility.

During its go-go days, Uber aggressively expanded into almost every market across the globe. However, as both economic and regulatory pressures mounted, it was forced to exit many of those markets as it couldn’t compete against the hyperlocal network effects other platforms had created.

For example, Uber sold its Southeast Asia business to competitor Grab in exchange for a 27.5 percent stake in the company. Two years prior, in 2016, it admitted defeat in China after losing over $1 billion a year to compete with Didi.

In other jurisdictions, it managed to establish a strong foothold. Uber acquired Dubai-based Careem for $3.1 billion in May 2019, allowing it to become the de-facto ride-hailing option across the whole Middle Eastern region.

Potential entrants would now have to spend billions in driver and rider incentives to acquire meaningful market share. Most investors wouldn’t be willing to see that through, leaving mostly Uber’s biggest competitors, including Didi or Ola, as potential threats.

However, those costly acquisitions are also one of the biggest reasons why Uber remains unprofitable to this day.

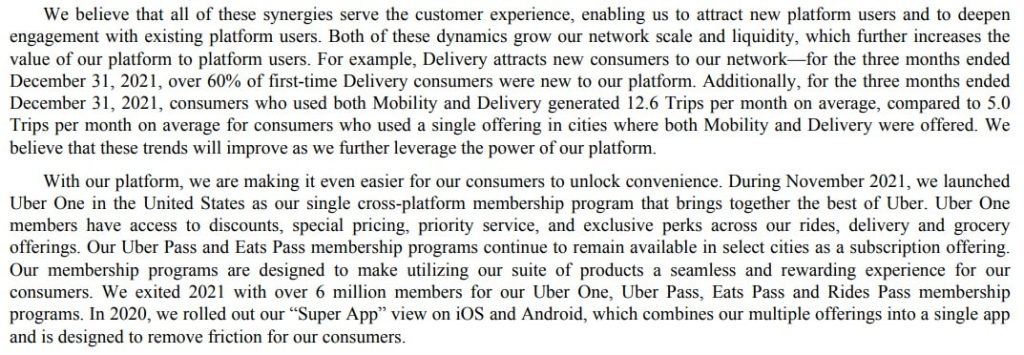

The other benefit of Uber’s network effects is its ability to cross-sell customers into other products and services. Uber has been running its food division (Eats) since 2014 and has since expanded into freight as well.

It currently is in the early stages of becoming a transportation super app. It first merged the Eats and Ride offerings into one single app and now added trains, buses, planes, and car rentals via Uber Explore (currently trialing in the UK).

And once again, its network economies come into play. At the height of the pandemic, Uber was able to shift portions of its existing driver supply to start delivering food instead. Since it had the driver’s contact data, Uber likely didn’t have to spend as much to acquire them anymore.

Moreover, each customer becomes more engaged with each additional offering that Uber launches. The company pointed out the benefits of the super app strategy during its 2021 Annual Report:

Customers that use both Ride and Food Delivery complete 12.6 transactions per month on average versus the 5 trips that users only accessing one offering purchase.

As Uber becomes more entrenched in its users’ lives, its ability to make money via associated services also increases. After all, a customer that regularly accesses Uber is more likely to pay for its premium subscription One.

The network effects also come into play during negotiations with its super app partners. An airline or train operator, when agreeing to advertise on Uber’s platform, will gain access to millions of additional users who (mostly) trust Uber.

Uber is likely able to charge higher commissions because of its ability to direct those millions of users into specific offerings.

2. Process Power

Another competitive moat that Uber possesses is process power, which means that the company is able to offer a superior product and/or lower costs due to the processes and/or technology it established.

Process power can only be attained through an extended commitment, which normally means being willing to pour significant funds into said process.

Uber famously wasted billions in hopes of replacing its drivers with autonomous vehicles only to shut down and sell off the division in December 2020.

However, there are still process power advantages that Uber possesses to this day. In the previously-mentioned S-1 prospectus, Uber was adamant to point out its technological superiority.

The company stated that it had “built proprietary marketplace, routing, and payments technologies” while it created a machine learning-based platform “that powers hundreds of models behind our data-driven services across our offerings and in customer service and safety.”

There’s at least some data to back up those claims. For example, Uber has filed over twice as many patents as its biggest competitor Lyft.

Furthermore, Uber’s research team is comprised of some of the world’s leading experts in AI and Computer Science. Prior to moving away from autonomous driving, it regularly published research papers that highlighted its advancements in computer vision, natural language processing (NLP), and associated fields.

For instance, Uber is able to automatically process millions of driver licenses and restaurant menus thanks to the algorithms its research team has developed.

Its technological prowess became evident just a year into launching the business. One of the innovations that Uber introduced was surge pricing, which algorithmically increases fares in times of excess demand.

Additionally, Uber utilizes so-called batch matching to find the most suitable driver for any given ride. That means Uber’s algorithms don’t just assign the closest driver but are optimizing for a variety of data points including ratings, vehicle types, and so forth.

This is also where Uber’s network economies come into play once again. The more vibrant the network is, the more rides are being completed, which in turn allows Uber to capture even more data.

As a result, its algorithms can learn everything they need about both the driver as well as the rider to make more tailored suggestions.

Additionally, the app itself can make recommendations on where riders should wait for their car. This is particularly important since many cities, such as Kuala Lumpur or Dubai, have malls and other buildings that can complicate the pick-up process.

In recent times, Uber also introduced new algorithms that improve the driver’s experience. For instance, a so-called trip radar lists all nearby ride requests (thus giving drivers choice) while upfront fares transparently show how much a driver will earn on any given trip.

All of these algorithmically-driven changes consequently enable Uber to increase its take rate, which unfortunately doesn’t always land in the drivers’ pockets.

3. Branding

Branding is the third competitive moat that Uber possesses. According to Helmer, a company with branding power enjoys a greater perceived value, which thus allows it to charge higher prices compared to similar offerings.

A brand is able to charge higher prices due to two reasons:

- Affective valence: the brand elicits good feelings, distinct from the objective value it brings to the table

- Uncertainty reduction: customers can have peace of mind knowing that the money they pay will be well spent

Unfortunately, data on whether Uber is indeed charging higher prices than its competitors is not available. However, there are a few indicators that point toward the strength of its brand.

First, though, it has to be noted that many see ride-hailing as a quasi-commodity, meaning that the product is effectively interchangeable.

Indeed, many customers often compare prices among the different platforms and often simply book the cheapest option. More precisely, 73 percent of all Uber riders name price as the most important factor in their booking decision.

As a result, companies have to separate themselves from the pack. The above-mentioned focus on technology is one. The other? Branding.

63 percent of all Uber customers say that they choose the platform due to the brand’s reputation. Interestingly, Lyft, which is often touted for its beloved brand, only scores 1 percent above Uber (63 percent).

While Uber’s and Lyft’s perceived value in the United States is essentially the same, that doesn’t apply to the 70+ other countries in that Uber operates.

Apart from Lyft, Uber also competes against the likes of Didi, Ola, inDriver, Bolt, Grab, and Cabify, among others.

As previously stated, one of the clearest indicators of brand power is the ability to charge higher prices for the same service. This naturally applies to the driver fees as well. Here’s what competing ride-hailing platforms charge drivers:

- Bolt: between 15 percent and 20 percent

- Grab: maximum of 20 percent

- inDriver: between 5 percent to 8 percent

- Didi: between 5 percent and 20 percent

- Ola: 18 percent

- Cabify: undisclosed

Uber, at roughly 30 percent, is thus able to charge substantially more to drivers. In all likelihood, portions of those higher costs are then passed onto the consumer (to allow drivers to earn at competitive rates and not switch to other platforms).

Uber likely profits from uncertainty reduction, meaning customers are willing to pay a higher price because they know they’ll arrive comfortably and safely at the destination they aim to go to.

4. Counter Positioning

The last competitive advantage in this article is not necessarily one that Uber still possesses but which was nonetheless very critical in getting the service off the ground during its founding days.

Counter positioning means that the newcomer adopts a new (and often superior) business model that incumbents are not willing to pursue due to the potential of cannibalizing their existing cash cow.

The incumbent that Uber initially counter-positioned against were local taxi operators – something that is rooted in the company’s early days back in 2009.

As the story goes, co-founders Travis Kalanick and Garrett Camp had to pay $800 to hail a taxi in snow-struck Paris. Excessive prices weren’t the only issues that both consumers and taxi drivers had to grapple with, though.

Apart from paying hefty fees, customers also either had to either call in advance and hope that the cab shows up or wait for extended amounts of time (depending on the location) to get a ride.

Additionally, hailing a cab was not without its dangers as there were no digitized records of who was driving who at what time.

However, where the counter positioning really came into play was on the taxi operator’s side. San Francisco, where Uber is headquartered, limited the number of taxi licenses to 1,500 for multiple decades.

New York City was even worse. The cost of a limited taxi license, also called a medallion, rose from $195,000 in 2001 to $600,000 in 2007 alone. Many taxi drivers seeking to branch out on their own even had to take out loans from predatory lenders.

As a result, the existing taxi operators in cities like New York or San Francisco had literally no incentives to upend the system that allowed them to overcharge customers for decades.

Interestingly, while Uber initially counter-positioned itself against taxi operators, it would later lose customers to platforms that did the same.

The most notable example is Lyft, its fiercest competitor in the US. While Uber was juggling from scandal to scandal (remember the #DeleteUber movement?), Lyft marketed itself as a platform for socially conscious consumers as exemplified by its slogan “your friend with a car.”

Uber, under the new leadership, has since done its best to distance itself from its troubled past by focusing on inclusivity, diversity, and being in compliance with local regulations.