Executive Summary:

Earnin is a platform that gives its users access to loans without the need of paying fees or interest. Users can borrow up to $500 at a time.

Earnin makes money via the tips it collects when issuing loans as well as through cashback rewards (offered by linking up your debit or credit card).

Founded in 2012, Earnin has become one of the leading platforms in the short-term loan space. The company has raised over $190 million in venture capital funding to this date.

How Does Earnin Work?

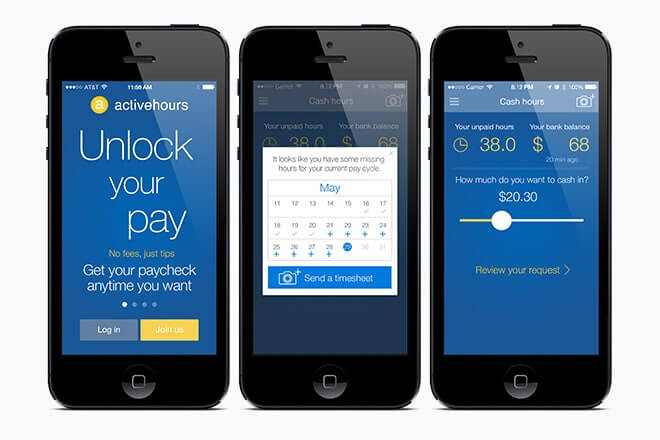

Earnin is a paycheck platform that allows you to borrow money without paying fees or interest. Customers can use their next paycheck as collateral to get money the same day.

Earnin works by automatically retrieving the amount you borrow from your checking account on your next payday.

The platform is built on a community-basis, meaning its members can support Earnin as well as each other by donating a fraction of their loan.

Earnin analyzes a few data points, such as the user’s GPS location (to check how often and long they’re at their workplace), to assess the likelihood of repayment.

To be able to use Earnin, users need to possess direct deposit access to a checking account set up by their employer, have consistent payment periods (such as weekly or monthly), and work at an identical location every day.

Users can access and retrieve a maximum of $100 per day. No more than $500 can be retrieved per pay period.

Apart from getting payments in advance, Earnin users can also earn cashback rewards, monitor their checking balance, and tip themselves.

Earnin is available via the firm’s website as well as on Android and iOS devices. A user’s credit score does not affect their eligibility to access the service.

Earnin Company History

Earnin, headquartered in Palo Alto, California, was founded in 2012 by Ram Palaniappan, who leads the company as CEO to this date.

Palaniappan, who came to the United States in the mid-1990s to pursue his MBA at Purdue, is certainly no stranger to the world of FinTech.

Before starting Earnin, he held various positions at a company called UniRush LLC. UniRush’s most notable product became the RushCard, a prepaid debit card led by legendary hip hop mogul Russell Simmons.

RushCard could essentially be described as the Earnin of the pre-digital age. It charged users $9.95 a month to hold their cash and $2.50 for ATM withdrawals while being branded to young and less affluent consumers.

RushCard was sold to Green Dot Bank for $147 million in January 2017 – but Palaniappan was already off to bigger and better things, though.

The spark that initiated the idea for Earnin actually arose from his work at UniRush. His colleagues would often have to take out payday loans (which are known to charge extremely high interest and are even forbidden in certain states) to make ends meet.

Knowing that they had a steady job and income, Palaniappan would simply loan the money out to them without charging any fees or interest. What he discovered was essentially everyone was able to pay back those small advances.

He, along with a few RushCard members, ended up leaving UniRush in 2012 to work on Earnin full-time.

It took his team over a year to figure out all the necessary building blocks. After all, the platform needed to be able to access employment data as well as integrate with various banking systems.

After months of alpha testing, Palaniappan and team released an Android and iOS app, respectively, in May 2014. Back then, Earnin was launched under the brand name Activehours (and was only rebranded as Earnin in 2017).

The firm’s quick access to money as well as its voluntary tipping system became a quick hit with consumers and investors alike. In 2017 and 2018, Earnin was able to add over $185 million in venture funding to its balance sheet.

By that time, employees from over 15,000 companies in the United States had gained access to Earnin’s financing solution.

The firm’s steady growth came at a cost, though. By 2019, the media started turning against Earnin, claiming that its marketing and business model resembled the one of a modern-day payday loan company.

Lauren Saunders, associate director of the National Consumer Law Center, said in an interview with the New York Post that Earnin was using a tipping (or pay as you go) system so they wouldn’t have to publicly disclose an APR (annual percentage rate). Yet, a $5 tip on a 4-day repayable $100 loan would be equal to a 456 percent APR.

Second, Earnin deployed the same marketing tactics that were used to great success at RushCard. The firm would try and get endorsements from African American celebrities like Nas (who also invested in the company) or T.D. Jakes to make the firm more approachable to low-income minority groups (which were often the ones targeted by traditional payday companies).

Third, Earnin’s software was experiencing frequent glitches and other issues. For instance, the app would just take out money from the user’s bank account even though there was no loan application being made.

It, therefore, came as no surprise when New York regulators announced that they’ve launched an investigation into the firm’s business practices. Furthermore, thousands of its users had filed a class-action lawsuit against the company.

In their complaint, the plaintiffs argued: “Earnin’s operations, along with its deceptive and incomplete disclosures, means that users like the Plaintiffs end up losing huge portions of their scarce wages to bank fees, which Earnin falsely assures users they will not receive.”

Earnin agreed to settle the lawsuit for $12.5 million. The company, furthermore, promised to completely overhaul its marketing to remove any form of deception.

Despite those hiccups, Earnin has continued to ascend in popularity over the past few years. In May 2020, it launched a B2B program that would see the company forming closer bonds with employers to offer them Earned Wage Access (EWA) benefits.

Today, more than 200 people are employed by Earnin, which operates out of offices in Palo Alto and Vancouver. The firm is ranked frequently among the most downloaded and used apps in the personal finance space.

How Does Earnin Make Money?

Earnin makes money via tips as well as cash ack rewards. Let’s have a closer look at both of those income streams below.

Tips

The vast majority of the income that Earnin generates comes from the tips its members give. These tips are given on a voluntary basis. Uses are thus not required, but heavily encouraged to tip.

Earnin utilizes concepts of behavioral psychology to entice users to tip. For instance, users are prompted to tip, not for themselves but to help the members of Earnin’s community.

As previously stated, the firm’s tipping policy came under intense scrutiny and even led to a $12.5 million settlement (as a result of a class-action lawsuit filed against the company).

A 2019 article by NBC News highlighted that Earnin was facilitating about $212 million per month through its platform. Moreover, 80 percent of its users leave a tip, equating to monthly revenue numbers of $8 million.

Earnin essentially operates on a so-called freemium business model, which means that the platform can be used free-of-charge (while offering additional payment options).

In recent years, the firm has focused on expanding the touchpoints with which a user can tip. For instance, Earnin introduced a B2B program (working together with employers) to ease the validation process.

With HealthAid, Earnin works together with medical providers to reduce a user’s unpaid medical bill. Users can then tip the company for negotiating on their behalf.

Cashback

In May 2019, Earnin introduced cashback rewards to its community. With cashback rewards program, members can earn up to 10 percent cash back at over 10,000 participating restaurants and retail stores.

Users can connect their personal debit or credit card in the Earnin app and automatically earn rewards whenever they shop. Almost 400,000 existing users joined the waitlist when the product was announced.

Earnin then generates revenue via the affiliate commissions that participating stores pay out. These normally range between 3 to 10 percent.

Offering cashback rewards can be highly advantageous to businesses. They can often attract new consumers or even entice them to become repeat customers.

Earnin Funding, Valuation & Revenue

According to Crunchbase, Earnin has raised $190.1 million across 4 rounds of venture capital funding.

Notable investors are Spark Capital, Andreessen Horowitz, Ribbit Capital, DST Global, or Matrix Partners, amongst others.

Earnin is currently being valued at around $800 million according to Forbes magazine. Revenue numbers, as with any other private company, are not disclosed as of today.